Introduction

A customer picks up a jar of your honey, admires your fresh produce, then asks, "Do you take cards?" When you shake your head no, they set everything down and walk away. This scenario plays out at farmers markets across the country, and it represents real money left on the table. Cash-only vendors risk losing significant sales to customers who rarely carry cash anymore — and that share of shoppers keeps growing.

This guide is for vendors at farm markets, garden centers with market stalls, and specialty food sellers who want a complete, practical understanding of credit card processingfrom the ground up. You'll learn how the payment process actually works, what equipment and setup it requires, what it costs, and how to choose the right solution for your operation.

Key Takeaways

- Credit card processing at a farmers market uses a mobile card reader, smartphone, and payment app—no fixed terminal or wired internet required

- Most vendors use mobile processors like Square (2.6% + $0.10/transaction) for low upfront costs and reliable offline mode

- On an $8 sale, expect to pay about $0.36 in fees, leaving most of your margin intact

- Multi-booth vendors benefit from integrated POS systems that handle inventory, sales reporting, and multiple payment types

- Market rules, SNAP/EBT eligibility, and connectivity conditions affect which setup works for your situation

What Is Credit Card Processing at a Farmers Market?

Credit card processing is the system that authorizes, captures, and transfers payment from a customer's card to your bank account. At a farmers market, this happens wirelessly using a mobile card reader paired with a smartphone or tablet and a payment processing app.

Unlike traditional retail, farmers market setups have no fixed internet connection, no hardwired terminal, and no permanent checkout counter. The entire system must be portable, battery-powered, and capable of handling intermittent mobile data.

Card Reader vs. POS System: What's the Difference?

- Mobile card reader: Accepts cards and processes transactions — nothing more

- Integrated POS system: Handles payments plus inventory, sales history, customer data, and reporting

The right choice depends on your volume. A card reader works fine for a single booth selling a handful of products. Once you're tracking dozens of SKUs or managing a farm market with multiple vendors, a full POS system pays for itself in time saved.

Why Accepting Credit Cards Matters for Farmers Market Vendors

Customers Have Gone Cashless

41% of Americans make no purchases with cash in a typical week. Cash now accounts for just 14% of all payments. When you operate cash-only, you're effectively turning away nearly half your potential customers before they even reach your booth.

Card Payments Prevent Lost Sales

Research specific to farmers markets shows that 28% of consumers have abandoned a purchase because their preferred payment method wasn't accepted. That's more than one in four potential buyers walking away empty-handed. Another 54% of shoppers say they'd be more likely to buy if credit cards were an option.

Transaction Values Increase Significantly

Customers spend substantially more when paying with cards:

- Credit card average transaction: $68 — more than 2.5x the cash average

- Debit card average transaction: $45 — 73% higher than cash

- Cash average transaction: $26

Over a full market season, that gap compounds into a meaningful revenue difference.

Impulse Purchases Drive Revenue

Many farmers market purchases are unplanned. A customer sees your fresh tomatoes or homemade jam and decides to buy on the spot. When cash is the only option, you lose the impulse buyer who doesn't happen to have bills in their wallet — and those buyers are often your most valuable ones.

You're Competing Against Card-Accepting Vendors

Most vendors at established farmers markets now accept cards. A cash-only booth puts you at a measurable disadvantage compared to vendors who accept cards — and shoppers notice.

How Credit Card Processing Works at a Farmers Market Booth

Here's the plain-language flow of a card transaction:

Customer presents card or device → card reader captures payment data → data is sent (or queued offline) to the payment processor → processor contacts the card network and issuing bank → authorization is returned → funds are deposited into your account within 1-2 business days.

Who Gets Paid (and Why You Pay a Fee):

- Payment processor (Square, Stripe, PayPal): Routes your transaction and manages settlement

- Card network (Visa, Mastercard): Provides the infrastructure connecting banks

- Issuing bank: The customer's bank that approves or declines the transaction

The processing fee covers the cost of routing through this network.

Step 1: Card Data Capture

Modern card readers handle three capture methods:

- Tap (NFC contactless): Fastest method, preferred at busy outdoor booths

- Chip insertion (EMV): High security, slightly slower

- Magnetic swipe: Backup method for older cards

Step 2: Authorization (Online or Offline)

With live data connection: The transaction is authorized in real time. The processor contacts the card network and issuing bank immediately, and approval comes back within seconds.

In offline mode: The transaction is stored locally on the device and submitted when connectivity is restored. Offline mode exists specifically for farmers markets with spotty or no cell signal.

Offline mode sounds convenient, but it comes with real trade-offs:

- You assume 100% of the risk — declined or disputed payments won't be recovered after the fact

- Funds aren't guaranteed until the transaction clears when connectivity returns

- Most processors limit offline mode to magnetic swipe only; chip and tap require a live connection

Step 3: Settlement and Deposit

Once authorized transactions are batched and submitted, the payment processor deducts its fee and deposits the net amount — typically within one business day. Square and Stripe typically hit your bank account the next morning. You can track every deposit in your app dashboard.

Choosing the Right Payment Setup for Your Farmers Market

Three Tiers of Payment Systems

1. Basic mobile card reader with free or low-cost app Best for: Single-booth vendors with simple product lineups and low transaction volume

2. Mid-tier mobile POS with inventory and reporting Best for: Vendors managing multiple product lines or operating at several markets per week

3. Full retail POS system Best for: Operations scaling beyond a single booth, managing seasonal inventory, or running year-round retail locations alongside market stalls

Comparing Leading Mobile Processors

| Processor | Card-Present Fee | Hardware Cost | Offline Mode | Monthly Fee |

|---|---|---|---|---|

| Square | 2.6% + 15¢ | $59 | Yes | No |

| PayPal Zettle | 2.29% + 9¢ | $29 (first reader) | Yes | No |

| Stripe Terminal | 2.7% + 5¢ | $59 | Yes | No |

All three use flat-rate pricing with no monthly fees on basic plans — a practical fit for seasonal vendors who want predictable costs without annual commitments.

Essential Hardware for Your Booth

Must-have equipment:

- Chip-and-tap card reader

- Charged smartphone or tablet

- Portable battery pack (non-negotiable, not optional)

Pro tip: Mount the reader at a fixed, customer-facing position rather than passing it back and forth. This speeds up the line and reduces handling errors.

The Cash-Plus-Card Hybrid Setup

Most vendors benefit from accepting both payment types:

- Start with a recommended cash float ($50-$100 in small bills)

- Use whole-dollar pricing to minimize coin handling

- Track cash sales in the same system as card sales for clean end-of-day reconciliation

Scaling Beyond Basic Card Readers

When you're juggling multiple product lines, seasonal inventory, and returning customers, a mobile card reader starts to show its limits. NCR Voyix Counterpoint, available through AMS Retail Solutions, is built specifically for farm markets and garden centers — covering inventory management, sales reporting, offline capability, and customer loyalty tools in a single system.

It also supports mobile checkout and consolidated reporting across multiple market locations, which basic readers handle poorly or not at all.

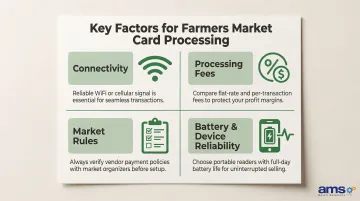

Key Factors That Affect Farmers Market Card Processing

Four variables determine whether card processing works smoothly at a farmers market — or becomes a problem you're troubleshooting in front of customers.

- Connectivity: Outdoor venues with weak cell signal require a processor with a proven offline mode. Test it before market day, not during it.

- Processing fees: Flat-rate pricing (like Square's 2.6% + 15¢) suits low-volume vendors. Interchange-plus pricing becomes worthwhile above roughly $100,000 per year, since you'll benefit from lower debit interchange rates and can negotiate the processor's markup.

- Market-specific rules: Many farmers markets prohibit card minimums, carry SNAP/EBT requirements, or run centralized token systems. Check your vendor agreement before setting up any payment hardware.

- Battery and device reliability: A dead phone mid-market shuts down card processing entirely. Bring a portable battery pack — it's as essential as your card reader.

Common Misconceptions About Farmers Market Payments

"Processing Fees Make Card Acceptance Unprofitable for Small Transactions"

Let's do the math on a typical low-value transaction. On an $8 sale using Square's 2.6% + 15¢ fee structure:

- Fee amount: $0.36

- Your net payout: $7.64

Compare that $0.36 cost to losing the entire $8 sale. Even on small transactions, the fee is modest relative to the alternative of no sale at all.

"Internet Connectivity Is Required at All Times"

Many vendors avoid card processing because they've experienced connectivity issues. Offline mode eliminates this barrier by storing transactions locally and submitting them automatically once signal is restored. The key is enabling offline mode before leaving for the market.

"I Need Expensive Hardware to Accept Cards"

A basic card reader from Square or PayPal costs $29-$59, and the app is free. That's the complete startup cost for accepting cards. That said, a basic reader has limits. Vendors managing inventory across multiple SKUs or running customer loyalty programs typically outgrow it quickly — a full POS system adds the reporting and inventory tracking that a standalone reader can't provide.

Frequently Asked Questions

How can farmers market vendors accept credit card payments?

Vendors use a mobile card reader (such as Square or similar) paired with a smartphone and payment app. No fixed internet or wired terminal required—the reader connects via Bluetooth and the app handles the transaction.

What is the cheapest way for a farmers market vendor to accept card payments?

Square offers a free magstripe reader (swipe-only), though the $59 contactless reader is recommended for tap payments. For low-volume vendors, flat-rate processing with no monthly fees usually costs less than subscription models.

Do I need internet access to process credit cards at a farmers market?

No. Offline mode queues transactions locally on the device when there's no signal and submits them automatically when connectivity is restored. Enable offline mode before leaving for the market.

Can farmers market vendors accept SNAP/EBT payments?

Yes, but it requires separate USDA FNS authorization. Many markets run a centralized EBT terminal, or individual vendors can apply through MarketLink for a free combined EBT/debit/credit device with no transaction fees.

What processing fees should farmers market vendors expect?

Typical flat-rate structures range from 2.29% to 2.7% plus 5¢ to 15¢ per transaction. On a $20 sale using Square (2.6% + 15¢), you'd pay $0.67 in fees and receive $19.33.

Should I use a simple card reader or a full POS system at my farmers market booth?

A basic card reader works for vendors with a simple product lineup and low volume. A full POS system makes sense once you're managing multiple SKUs, tracking inventory, running loyalty programs, or selling across multiple market locations.